Balanced Scorecard is a strategic planning and management system used to align business activities to the vision statement of an organisation. Balanced Scorecard attempts to translate the sometimes vague, pious hopes of a company’s vision/mission statement into the practicalities of managing the business better at every level. According to Gem-Up Consulting Inc (2009), the Balanced Scorecard principles were developed by Robert Kaplan (Accounting professor at Harvard University) and David Norton (Consultant from Boston).

In Barron’s Accounting Dictionary, Balanced Scorecard is defined as an approach to performance measurement that also focuses on what managers are doing today to create future shareholder value. A balanced scorecard is a set of performance measures constructed for four dimensions of performance. The dimensions are financial, customer, internal processes, and learning and growth.

Having financial measures is critical even if they are backward looking. After all, they have a great effect on the evaluation of the company by shareholders and creditors. Customer measures examine the company’s success in meeting customer expectations. Internal process measures examine the company’s success in improving critical business processes; while learning and growth examine the company’s success in improving its ability to adapt, innovate, and grow. The customer, internal processes, and learning and growth measures are generally thought to be predictive of future success (i.e., they are not backward looking).

After reviewing these measures, note how ‘balance’ is achieved:

- performance is assessed across a balanced set of dimensions (financial, customer, internal processes, and innovation);

- quantitative measures (e.g., number of defects) are balanced with qualitative measures (e.g., ratings of customer satisfaction); and

- there is a balance of backward-looking measures (e.g., financial measures like growth in sales) and forward-looking measures (e.g., number of new patents as an innovation measure).

To embark on the Balanced Scorecard path, an organisation first must know (and understand) the following:

- The company’s mission statement; and

- The company’s strategic plan/vision

Then:

- The financial status of the organisation

- How the organisation is currently structured and operating

- The level of expertise of their employees; and

- Customer satisfaction level.

Once an organisation has analysed the specific and quantifiable results of the above, they should be ready to utilise the Balanced Scorecard approach to improve the areas where they are deficient. The metrics set up also must be SMART (commonly, Specific, Measurable, Achievable, Realistic and Timely) – you cannot improve on what you can’t measure! Metrics must also be aligned with the company’s strategic plan.

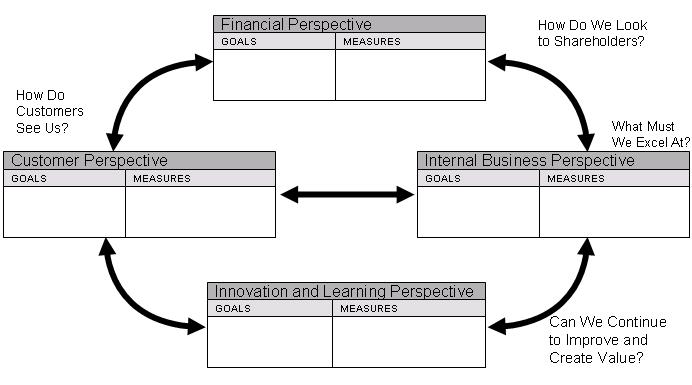

A Balanced Scorecard approach generally has four perspectives: Financial, Internal business processes, Learning & Growth (human focus, or learning and development), and Customer. Gem-Up Consulting Inc stated further that the original methodology broke-down the Balanced Scorecards into 4 perspectives as follows:

- Financial, in order to measure the economic consequences of the strategy.

- Customer, to summarise the value proposition offered to customer.

- Internal Business Process, to measure the efficiency of the processes implemented to meet the value proposition.

- Learning and Growth, to consider the important internal skills, capabilities and assets to support the value-creation process.

Kaplan and Norton’s original Balanced Scorecard design (Cobbold & Lawrie, 2002)

Balanced scorecard – factors examples

Finance · Return On Investment · Cash Flow · Return on Capital Employed · Financial Results (Quarterly/Yearly) | Learning & Growth · Is there the correct level of expertise for the job? · Employee turnover · Job satisfaction · Training/Learning opportunities |

Internal Business Processes · Number of activities per function · Duplicate activities across functions · Process alignment (is the right process in the right department?) · Process bottlenecks · Process automation | Customer · Delivery performance to customer · Quality performance for customer · Customer satisfaction rate · Customer percentage of market · Customer retention rate

|

Each of the four perspectives is inter-dependent – improvement in just one area is not necessarily a recipe for success in the other areas.

Balanced scorecards essentials (Gem-Up Consulting Inc, 2009)

How a balanced scorecard could help an organisation | Balanced scorecards combine strategy formulation and management in a single solution. Scorecards can help an organisation by communicating the business strategy in practical, easy to understand day-to-day activities. When implemented efficiently, balanced scorecards can be used as a business performance framework and help the organisation in many ways: · Break the miscommunication issues between management and employees. · Increase focus on results. · Understand better the causal-effect between business processes, people, client-facing activities and financials. · Help leaders prioritize the work and make timely decisions based on factual information. · Force the creation of a sound strategy, appropriate objectives and appropriate resourcing. · Help employees perform to their best. |

Reasons why SMBs benefit immensely from scorecards | A scorecard system is ideal for small and medium size businesses (SMBs) for the following reasons: · Scorecards require little training and simple tools. Their simplicity and easy implementation are seamless for SMBs where resources are often scarce, time is priceless and managers wear multiple hats. · SMBs need to measure their effort and focus only on opportunities that will take them closer to their business goals. SMBs are often rich of ideas because of the intimacy they have with their niche market. The temptation to chase all opportunities might be difficult to resist but often result in dispersion. Scorecards focus SMBs efforts. · SMBs are a lot less resilient to management errors than larger settings. Implementing a scorecard systems minimize errors while keeping management cost minimal. · SMBs are strong when they are reactive; they need a management system that permits near-real time analysis and fast strategy changes when needed. Yet at the same time SMBs need to communicate change to staff quickly and in the least onerous way. Scorecards are integrated and combine strategy, communication and change management in a single tool. · Scorecards, such as the balanced scorecards, have been researched for many years; they come with a knowledge base. When implementing Scorecards, SMBs do not need to reinvent the wheel; they get a head-start on basic practices and can focus on their differentiators and competitive advantages. |

Reasons for using management scorecards | The major benefits derivable from using a scorecard system in any organisation are: · You only do what you measure. At every level of an organisation (tactical, operational, strategic) practical experience proves that only the activities that are measured are actually implemented with strength, focus and determination. Scorecards are priority-management tools. · It keeps the organisation honest to itself. The fairness and honesty of Key Performance Indicators enforces that every decisions is made toward performance improvement, short and long term. Scorecards are analytical tools. · Scorecards have proven to be an efficient performance management technique and allow adopters to significantly improve their performance. Scorecards are performance management tools. · Short term decisions are kept in-line with the strategy. Scorecards enforce the mapping of tactical initiatives to approved strategy on a continuous basis. Scorecards are tactical tools. · Long term decisions and visibility are rationalised in scorecards. Scorecards capture the strategic decisions, their rational and sustainability. Scorecards are strategic tools. · Scorecards embed and regularly remind the organisation of its strategic objectives, dynamically and concisely. Scorecards are communication tools. · Scorecards enable the tracking of performance and the triggering of just-in-time agile decisions. Scorecards are decisions tools. · When the goals set by scorecards are achieved, it feels good. Scorecards are morale-booster tools. · Scorecards define clear rules and ownership of objectives. Scorecards are accountability tools. · Scorecards spark off business process improvement by isolating non-value add activities and delivering cause-effect analysis of your organisation, enabling reduction of poorly performing activities. Scorecards are cost-saving tools. |

Balance scorecard implementation

Implementing the Balanced Scorecard system company-wide should be the key to the successful realisation of the strategic plan/vision. A Balanced Scorecard should result in:

- Improved processes

- Motivated/educated employees

- Enhanced information systems

- Monitored progress

- Greater customer satisfaction

- Increased financial usage

There are many software packages on the market that claim to support the usage of Balanced Scorecard system. For any software to work effectively it should be:

- compliant with your current technology platform;

- always accessible to everyone – everywhere; and

- easy to understand/update/communicate

Feedback is essential and should be on-going and contributed to by everyone within the organisation. And it should be borne in mind that Balanced Scorecards do not necessarily enable better decision-making.

References

Balanced scorecard. (n.d.). Dictionary of accounting terms. Retrieved April 22, 2011, from Answers.com Web site: http://www.answers.com/topic/balanced-scorecard.

Cobbold, I. & Lawrie, G. (2002). The development of balanced scorecard as a strategic management tool. Paper presented at PMA Conference, Boston, USA, May 2002.

Gem-Up Consulting Inc (2009). Balanced scorecard. http://www.managementscorecards.com/resources/articles/scorecards-help-organisations.htm

Sandra McCarthy and Alan Chapman (2009). http://www.businessballs.com/balanced_ scorecard.htm