A capital lease is called a ‘finance lease’ by the IFAC. A finance lease or capital lease is a lease that transfers substantially all the risks and rewards incidental to ownership of an asset. According to Business Victoria (2008), finance leases are those in which the rights, duties and privileges of ownership reside with the lessee, who is really buying the asset over time and has borrowed finance in the form of leasing. Any property, plant and equipment, or motor vehicle, which is being acquired under a finance lease is accounted for in exactly the same way as any other purchased property, plant, or vehicle (that is, its initial cost at acquisition is recorded and this value is depreciated).

A finance lease is a lease that transfers substantially all the risks and rewards incidental to ownership of an asset. Title may or may not be eventually transferred. The following are regarded as features of finance lease:

- the lease transfers ownership of the asset to the lessee by the end of the lease term;

- the lessee has the option to purchase the asset on advantageous terms;

- the lease term is for the major part of the economic life of the asset even if title is not transferred;

- at the inception of the lease the present value of the minimum lease payments amounts to at least substantially all of the fair value of the leased asset;

- the leased assets are of such a specialised nature that only the lessee can use them without major modifications;

- if the lessee can cancel the lease, the lessor’s losses associated with the cancellation are borne by the lessee;

- gains or losses from the fluctuation in the fair value of the residual accrue to the lessee;

- the lessee has the ability to continue the lease for a secondary period at a rent that is substantially lower than market rent.

Under International Accounting Standard (IAS) 17, it is a requirement that leases be classified for inclusion in financial statements as either operating leases or finance leases. In this regard leases are classified as either finance or operating leases. Title may or may not be eventually transferred. (IAS 17, para. 4). It is a commercial arrangement where the:

- lessee (customer or borrower) will select an asset (equipment, vehicle, software);

- lessee has the option to acquire ownership of the asset (e.g. paying the last rental, or bargain option purchase price);

- lessee will have use of that asset during the lease;

- lessee will pay a series of rentals or instalments for the use of that asset;

- lessor (finance company) will purchase that asset;

- lessor will recover a large part or all of the cost of the asset plus earn interest from the rentals paid by the lessee.

In general, a finance lease (or capital lease) is one in which all the benefits and risks of ownership are transferred substantially to the lessee. The legal owner (the holder of the title) may still be the lessor. The finance company is the legal owner of the asset during duration of the lease. However the lessee has control over the asset providing them the benefits and risks of (economic) ownership. International Accounting Standard (IAS 17) has the following five tests. If any of these tests are met, the lease is considered a finance lease:

- ownership of the asset is transferred to the lessee at the end of the lease term;

- the lease contains a bargain purchase option to buy the equipment at less than fair market value;

- the lease term is for the major part of the economic life of the asset even if title is not transferred;

- at the inception of the lease the present value of the minimum lease payments amounts to at least substantially all of the fair value of the leased asset.

- the leased assets are of a specialised nature such that only the lessee can use them without major modifications being made

Operating lease

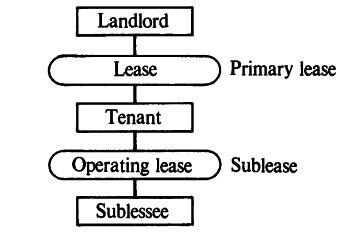

An operating lease is a lease other than a finance lease. For example, leases of part of a multi-let building will normally be operating leases and the whole property will be classified as investment property by the lessor. Operating lease is a lease between the lessee and the sublessee who actually occupies and uses the property; it is a lease contract that allows the use of an asset, but does not convey rights similar to ownership of the asset. An operating lease is not capitalised; it is accounted for as a rental expense. According to Business Victoria (2008), operating leases are those leases involving purely renting of the items. A hire car is an example, where the duration of the ‘lease’ is short term and the owner carries the responsibility of operation and maintenance of the asset.

Usually an operating lease assumes a reasonable length of time, that is, it is a long term lease, but in the lease there is no commitment to permanent use of the asset and the duration of the lease is not indefinite. In other words, the lease is long-term, but cancellable. Operating leases can vary, so that the lessee may take on more or less of the responsibility for maintaining the item leased (Business Victoria, 2008).

Under IAS 17, paragraph 4, an operating lease is defined as a lease other than a finance lease; it is a lease whose term is short compared to the useful life of the asset or piece of equipment being leased. An operating lease is commonly used to acquire equipment on a relatively short-term basis. For example, an aircraft which has an economic life of 25 years may be leased to an airline for 5 years on an operating lease. The determination of whether a lease is a finance (also called capital) lease or an operating lease is defined in the United States by Statement of Financial Accounting Standards No. 13 (FAS 13). In countries covered by International Financial Reporting Standards, the tests are defined in IAS 17.

Capital Leases vs. Operating Leases

An operating lease represents a rental agreement for an asset from lessor under the terms that GAAP does not require to record as a capital lease. The typical assets that are rented under operating leases include real estate, aircraft and various equipments with long useful life spans. To meet operating lease classification, companies must perform tests consisting of four criteria that determine whether rental contracts must be booked as operating or capital leases. For instance, the Financial Accounting Standards Board (FASB) has imposed some restrictions on which leases can be treated as operating leases. A lease must be treated as a capital lease if it meets any single oneof the following 4 conditions:

- Ownership: The lease transfers ownership of the property to the lessee by the end of the lease term.

- Bargain price option: The lease contains an option to purchase the leased property at a bargain price.

- Estimated economic life: The lease term is equal to or greater than 75 percent of the estimated economic life of the leased property.

- Fair value: The present value of rental and other minimum lease payments, excluding that portion of the payments representing executory costs, equals or exceeds 90% of the fair market value of the leased property.

The last two criteria do not apply when the beginning of the lease term falls within the last 25 percent of the total estimated economic life of the leased property. If none of these criteria are met and the lease agreement is only for a limited-time use of the asset, then it is an operating lease.

Unlike a finance lease, at the end of the operating lease the title to the asset does not pass to the lessee, but remains with the lessor. Accordingly, at the end of an operating lease, the lessee has several possibilities:

- Pursuit of the lease

- Return of the equipment

- Renewal of equipment

- Restoration of equipment

- Purchase of equipment at their market value.

Difference between finance lease (capital lease) and operating lease

An operating lease is treated like renting — payments are considered operational expenses and the asset being leased stays off the balance sheet. In contrast, a capital lease is more like a loan; the asset is treated as being owned by the lessee so it stays on the balance sheet. The accounting treatment for capital and operating leases is different, and can have a significant impact on taxes owed by the business.

Capital Lease versus Operating Lease comparison chart

Finance (capital) lease | Operating lease | |

Lease criteria – Ownership | Ownership of the asset might be transferred to the lessee at the end of the lease term. | Ownership is retained by the lessor during and after the lease term. |

Lease criteria – Bargain Purchase Option | The lease contains a bargain purchase option to buy the equipment at less than fair market value. | The lease cannot contain a bargain purchase option. |

Lease criteria – Term | The lease term equals or exceeds 75% of the asset’s estimated useful life | The lease term is less than 75 percent of the estimated economic life of the equipment |

Lease criteria – Present Value | The present value of the lease payments equals or exceeds 90% of the total original cost of the equipment. | The present value of lease payments is less than 90 percent of the equipment’s fair market value |

Risks and Benefits | Transferred to lessee. Lessee pays maintenance, insurance and taxes | Right to use only. Risk and benefits remain with lessor. Lessee pays maintenance costs |

Accounting | Lease is considered as asset (leased asset) and liability (lease payments). Payments are shown in Balance sheet | No risk of ownership. Payments are considered as operating expenses and shown in Profit and Loss statement |

Tax | Lessee is considered to be the owner of the equipment and therefore claims depreciation expense and interest expense | Lessee is considered to be renting the equipment and therefore the lease payment is considered to be a rental expense |

Advantages of finance (capital) lease and operating lease

References

Barron’s Accounting Dictionary. Dictionary of Accounting Terms. Copyright © 2010 by Barron’s Educational Series, Inc.

Barron’s Banking Dictionary. Dictionary of Banking Terms. Copyright © 2006 by Barron’s Educational Series, Inc.

Barron’s Real Estate Dictionary. Dictionary of Real Estate Terms. Copyright © 2008 by Barron’s Educational Series, Inc.

Closed-End Lease. (n.d.). Dictionary of Banking Terms. Retrieved July 07, 2011, from Answers.com Web site: http://www.answers.com/topic/true-lease

Closed-End Lease. (n.d.). Dictionary of Real Estate Terms. Retrieved July 07, 2011, from Answers.com Web site: http://www.answers.com/topic/true-lease

Closed-End Lease. (n.d.). Investopedia. Retrieved July 07, 2011, from Answers.com Web site: http://www.answers.com/topic/true-lease

Investopedia Financial Dictionary. Copyright ©2017, Investopedia.com- Owned and Operated by Investopedia USA Division of ValueClick, Inc.

Investopedia Financial Dictionary. Copyright ©2017, Investopedia.com- Owned and Operated by Investopedia USA Division of ValueClick, Inc.

Operating Lease. (n.d.). Dictionary of Accounting Terms. Retrieved July 07, 2011, from Answers.com Web site: http://www.answers.com/topic/operating-lease.

Operating Lease. (n.d.). Dictionary of Real Estate Terms. Retrieved July 07, 2011, from Answers.com Web site: http://www.answers.com/topic/operating-lease.

Operating Lease. (n.d.). Investopedia. Retrieved July 07, 2017, from Answers.com Web site: http://www.answers.com/topic/operating-lease

Operating lease. (n.d.). Wikipedia. Retrieved July 07, 2017, from Answers.com Web site: http://www.answers.com/topic/operating-lease-1

Diffen.com (2017). Capital lease vs. operating lease. http://www.diffen.com/difference/Capital_Lease_vs_Operating_Lease

Real Estate Glossary Business Dictionary Definition Head Lease”. www.bizoptions.com. http://www.bizoptions.com/glossary/h.asp. Retrieved 2010-08-05.